We expect continued volatility as markets adjust to the economic, legal and political uncertainties of the U.K.’s exit process. It is plausible that U.K. and European economic growth could face headwinds as a result of the uncertainty and as capital flows reflect the investor reaction. We expect that a prolonged exit and negotiation process will create a significant drag on UK exports and overall economic growth, and a smaller but material drag on EU growth. As European financials, insurance, U.K. economically sensitive equities and Sterling are the most direct way for markets to express their views, we expect acute volatility in these areas in particular.

Key US impacts are likely to include a more dovish Federal Reserve (Fed). From a policy perspective, the most predictable implication is that the Fed is likely to be on hold for the foreseeable future. Ahead of the U.K. vote, the Fed had already signaled a great deal of caution in its policy normalization plans, which the Brexit-related shock amplifies. The Bank of England, ECB and Bank of Japan could all contemplate moves, but we expect this to be highly dependent on the market reaction over the next few days and months.

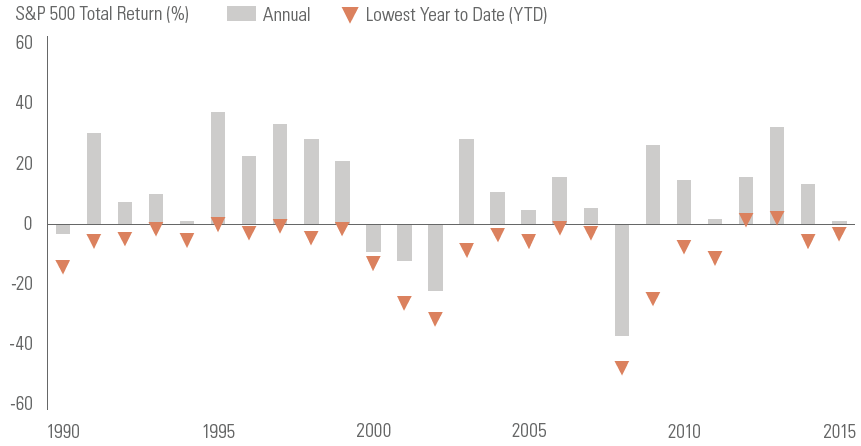

Selloffs are a normal investment experience. We would remind investors that shocks to the system are inevitable, and equity selloffs are historically frequent. In19 of 21 positive calendar-year returns since 1990, the S&P 500 spent some portion of the year in negative territory. For this reason, we see investors’ task as building in realistic assumptions for market turbulence. After an extended period of low volatility, markets may have entered a new phrase of more historically normal (higher) volatility.