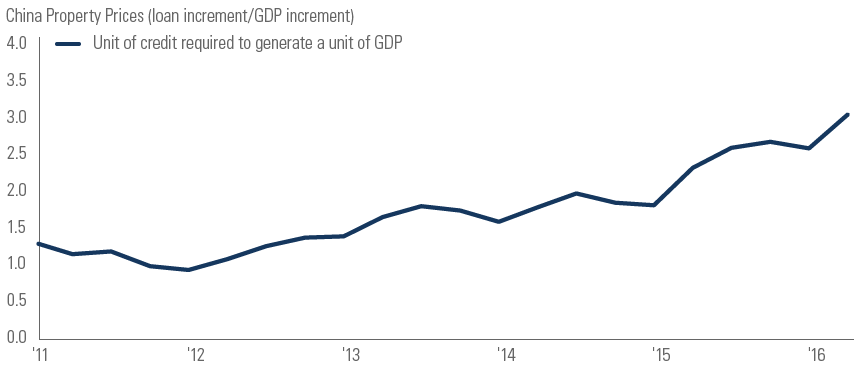

In our view, China’s current pace of credit and economic growth are ultimately unsustainable. Credit seems to be becoming less and less efficient at generating economic growth, requiring more and more loans to keep growth near the government’s target (Exhibit 1). Eventually, something has to give, but we think policymakers can continue to kick the can down the road for the foreseeable future.

The optimistic explanation for the declining efficiency of credit is that China’s economic transition, high savings and financial structure all support higher credit growth. In an export-oriented economy, a loan to a start-up company looking to sell goods abroad can boost economic output relatively quickly. The credit required to invest in a new subway line may not produce economic benefits for several years. Thus, as China has transitioned to an economy driven more by domestic demand and investment, credit expansion may simply be taking longer to flow through to economic growth. China’s high savings rate and relatively small equity market may also be contributing to debt growth, as savings flow to borrowers.

We think the optimistic case for China’s debt growth makes some sense, but we remain wary of the pace of new credit creation and the sustainability of existing debt. New credit is primarily flowing to infrastructure and real estate (which offers banks the security of collateralized lending). Much of the existing debt stock is held in the corporate sector. The bulk of this corporate debt was accumulated by state-owned enterprises (SOEs) controlled by local governments in sectors such as coal, steel and shipbuilding that are now burdened by excess capacity, weak profitability and declining efficiency.

Looking ahead, we think the growth of non-performing loans in excess-capacity sectors will increase pressure on the banking system, eventually requiring recapitalization. In our view, the most likely scenario is a relatively large recapitalization equivalent to around 30% of Gross Domestic Product (GDP), but through a process that is relatively benign and opaque. Much of the existing debt is owed by government-linked companies to government-linked banks. We think the government will need to inject capital, and some non-performing assets are likely to get shuffled around and adjusted in ways that buy time and limit stress in the banking system.

We think the best-case scenario (but also the least likely) is that policymakers enact reforms targeted at the local SOEs and shadow lenders and direct new credit to projects that increase potential growth. In that scenario, we think the need for recapitalization could be significantly smaller, perhaps equivalent to 10% of GDP.

The risk scenario is that new credit is directed to unproductive investment and capital outflows create a funding crisis that requires a bigger recapitalization. While not our base case, this is the scenario we watch for when looking to China for potential signs of disruptive change.