A diversified approach can help investors tap a range of drivers of investment return while also potentially reducing the relative highs and lows of any single smart beta strategy versus a market index.

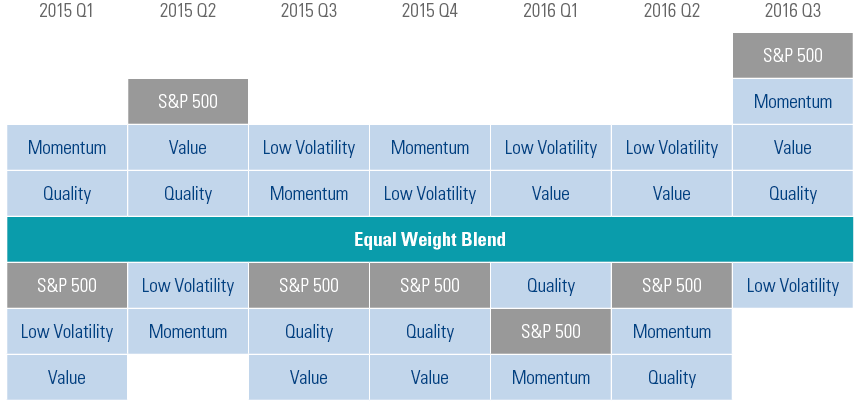

To test these views out, we examined how a diversified approach has played out recently. In Exhibit 1, we present Standard & Poor’s index returns for four widely followed smart beta investment characteristics: Momentum, Low Volatility, Quality, and Value (see endnotes for definitions and chart notes for index definitions), plus an equally apportioned blend of all four approaches.

The result: The equal-weight blend outperformed the S&P 500 Index the majority of the time, while also avoiding the relative highs and lows of individual smart beta approaches. This is consistent with our expectation that a blend of strategies may deliver a more consistent investment experience, at least in a relative sense versus market indices and versus a narrower smart beta exposure.