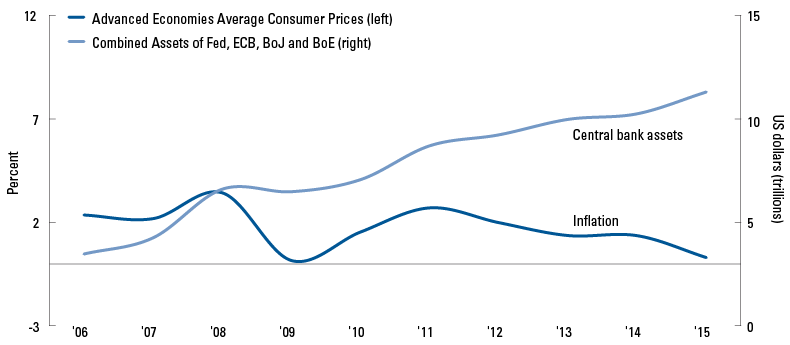

The new year opens on a significant shift in the global macro backdrop, with the US Federal Reserve (Fed) having raised interest rates. However, global monetary policy is likely to remain highly accommodative and we expect the global economy will maintain its course of positive, but sluggish, growth and low inflation.

These are benign—indeed, supportive—conditions for fixed income markets, but valuations in some sectors suggest investors are more focused on potential worst-case scenarios in growth and inflation, commodities and corporate credit, and emerging markets and China. These are grounds for concern and potential drivers of volatility in 2016, as we discuss in the following pages. However, we still see opportunities in select areas and relative value strategies.

- Our global economic outlook is still positive but softer than consensus, as broadly favorable trends in consumer demand and job creation are offset by weak external demand, capital expenditure and wage growth.

- We believe the Fed is likely to raise interest rates three times in 2016 if inflation picks up as expected. However, we think the Fed could move more slowly—in line with market expectations—if financial conditions tighten too much.

- On the easing side of policy divergence, we believe quantitative easing (QE) will remain a key policy tool for the European Central Bank (ECB) and Bank of Japan (BoJ) this year, but the limitations and drawbacks of this strategy are increasingly clear.

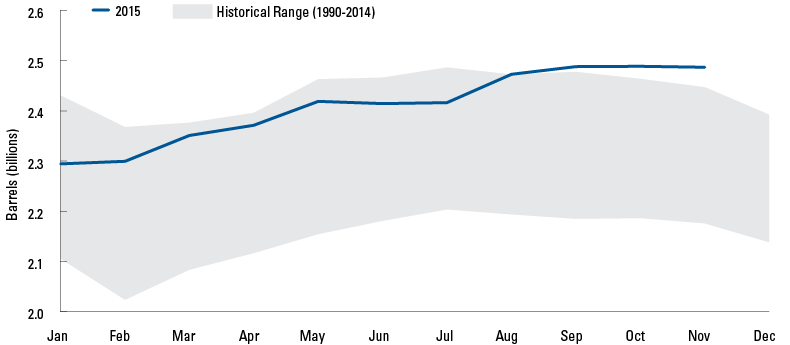

- The commodities market downturn doesn’t look likely to let up any time soon. We see potential for additional near-term downward pressure on oil prices due to concerns that storage is getting close to full capacity.

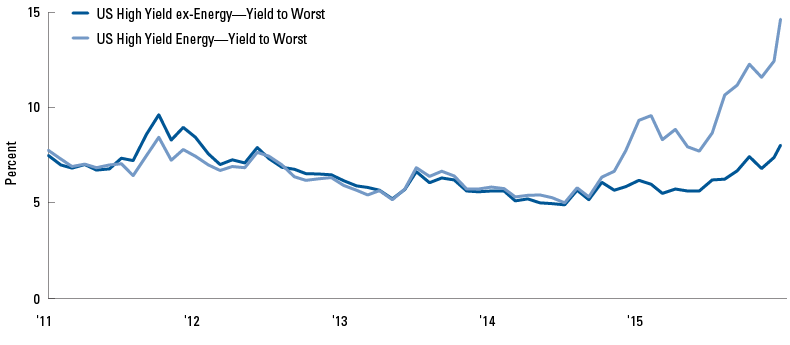

- We think the credit cycle has further to run but concerns are mounting as it advances into the late stage, and given the risk of contagion from the distressed energy and mining sectors. These concerns are keeping us from being more positive on risk assets, but we remain constructive on corporate credit as we think current valuations reflect an overly pessimistic scenario for the global economy and markets.

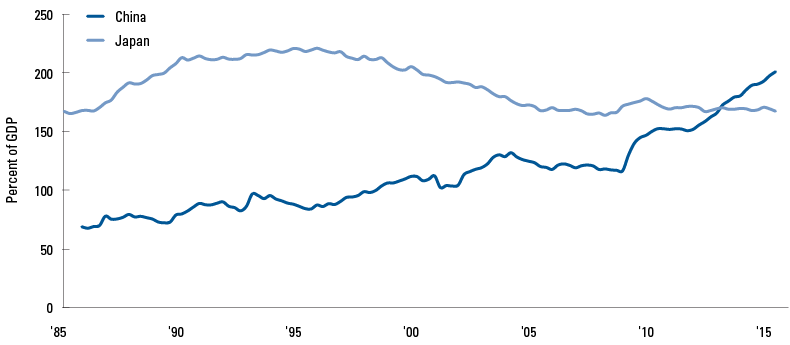

- Turning finally to the predominant market focus, our concerns about China haven’t changed,given the persistent risks of policy missteps, equity and currency market volatility and strong credit growth. The pressures of China’s competing objectives in the transition to a consumer-driven,market economy are evident, but we believe authorities are focused on containment, which may limitrisks to the global economy and markets.