Investor flows are the lifeblood of any market recovery, and this is no less true in the diverse spectrum of the emerging markets. Yacov Arnopolin, portfolio manager for GSAM’s Emerging Markets debt and currency team, has been tracking the tides and sees a positive turn thanks to a resilient strategic investor base.

Why are investor flows such a perennially hot topic in emerging markets debt?

We often get questions from investors concerning flows in and out of emerging markets debt. The typical narrative centers on the potential instability of “tourist money” that flooded the sector after the global financial crisis, seeking higher growth and an escape from the over-levered balance sheets of developed market countries.

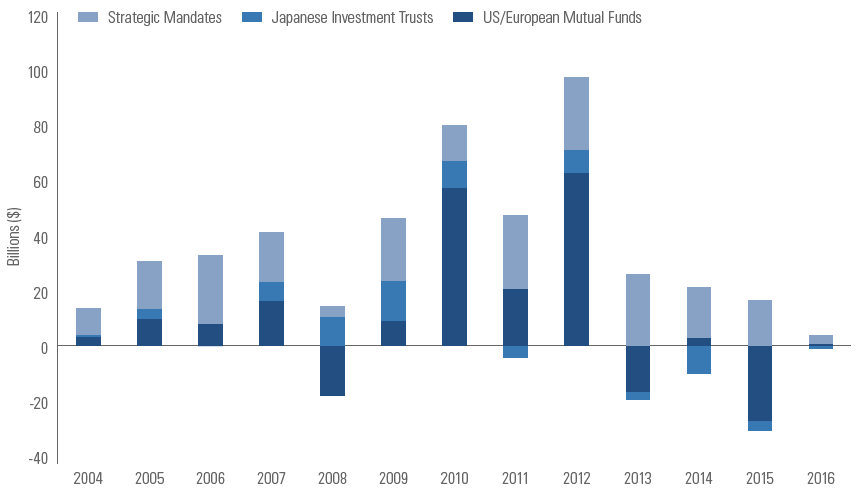

We recognize this ‘push’—out of quantitative easing—and ‘pull’—to countries on a sounder financial footing— but the story is more nuanced. The 2010-12 period saw a surge of retail money into emerging market debt mutual funds (see Exhibit 1). This may have been in part a corollary of the excitement around emerging market equities, with some of the money finding its way into fixed income. But the charm of emerging markets seemingly turned to a curse in 2013 with the “taper tantrum,” and many retail investors started to exit.

How did outflows impact performance and what are the implications in a recovery?

It is difficult to pinpoint how the fluctuation of fund flows since 2013 has impacted sector performance. However, just as negative returns often lead to outflows, positive returns lead to retail inflows—which may exacerbate the price action both on the upside and the downside. Whatever the case, we have observed retail outflows in the US and Europe slowing to a trickle, and overall flows have turned positive year-to-date. This leads us to believe most of the money that wanted to rush for the exits has already done so.

If all flows aren’t equal, how do you differentiate between the “tourists” and more committed investors?

We consider inflows by investor type. Over the past several years we’re encouraged by the steady pace of investment via ‘strategic mandates,’ reflected in segregated account funding by institutional investors. We continue to see a steady flow of client inquiries and Requests for Proposals, and flows data (see chart) chime with our impression of a consistent, gradual ramp-up of exposure.