How do you think about the probability of various scenarios for credit spreads in this environment?

For the rest of 2016, we think the most likely scenario is that the high yield market moves sideways. Near-term, the Italian constitutional referendum and the US presidential election could lead to higher volatility. However, compared to earlier this year, we assign marginally lower probability to the risk that political events will create a major turning point given central banks' ongoing commitment to stimulate markets and the relatively short-term impact of the UK's European Union referendum.

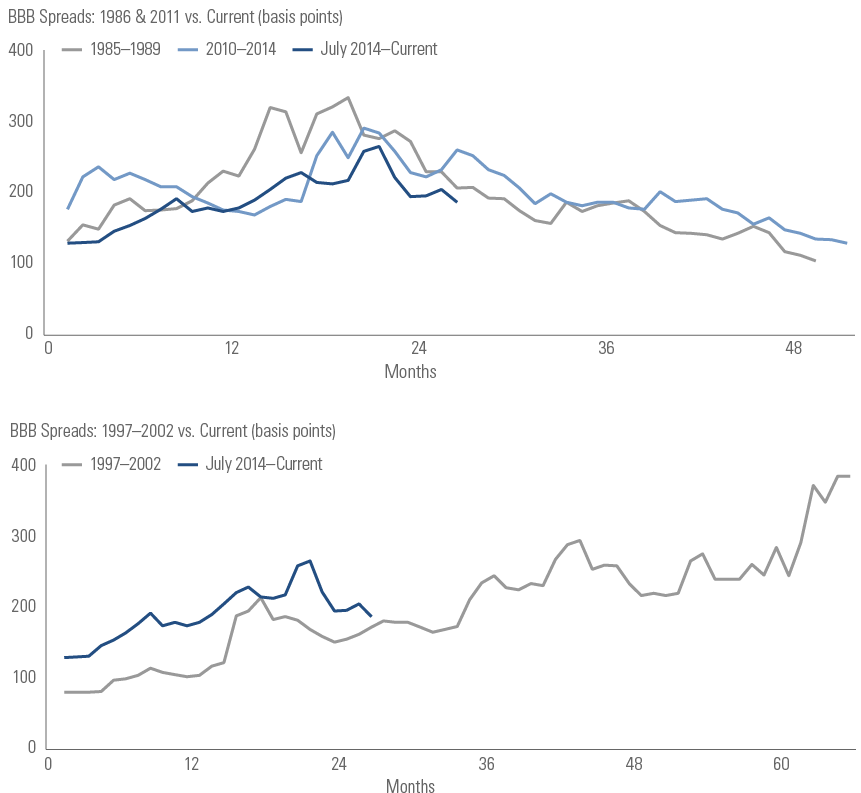

Over the longer-term, if we are wrong about credit being in the late cycle, spreads could continue to tighten for some time, as we saw in 1986 and 2011 (Exhibit 2, top chart). However, we think the more likely scenario is that the policy environment has created a temporary rally in a longer-term trend of wider spreads and underperformance, similar to the rallies that occurred in the 1997-2002 period (Exhibit 2, bottom chart). If that is the case, we believe now is not the time to reach for yield in the corporate bond sector.