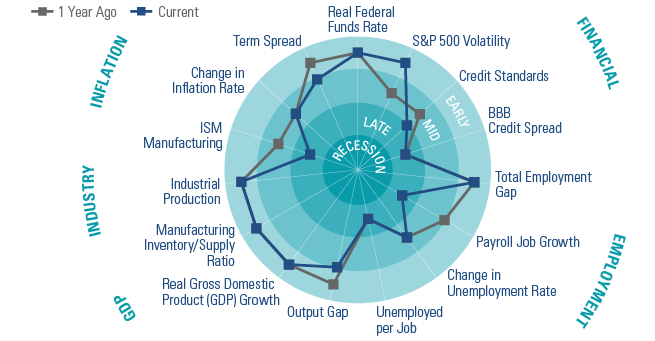

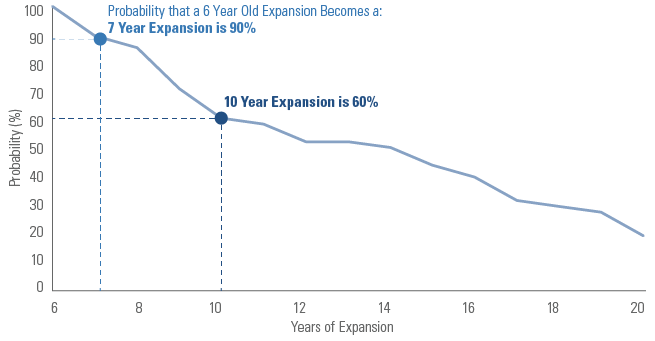

As the current six-year-old economic expansion rolls on, some investors may be focused on the age of the expansion. Here’s why we think that the current prolonged period of modest-but-positive global growth can continue.

In our view, several factors are supporting growth in developed economies. One is accommodative monetary policy. Both the Bank of Japan and European Central Bank remain in maximum accommodation mode, and interest rates in the US, though rising, remain low by historical standards. Moreover, as rates begin to rise in the US, we would point out that, historically, the start of a Federal Reserve tightening cycle has not ended the expansion phase of the US economic cycle, nor we do not expect that to happen this time around.1