Emerging market debt can help diversify a portfolio and serve as a tool in the pursuit of yield and attractive risk-adjusted returns. The late 2016 selloff has raised a question for some investors: Do rising US interest rates represent a new negative factor for emerging market debt?

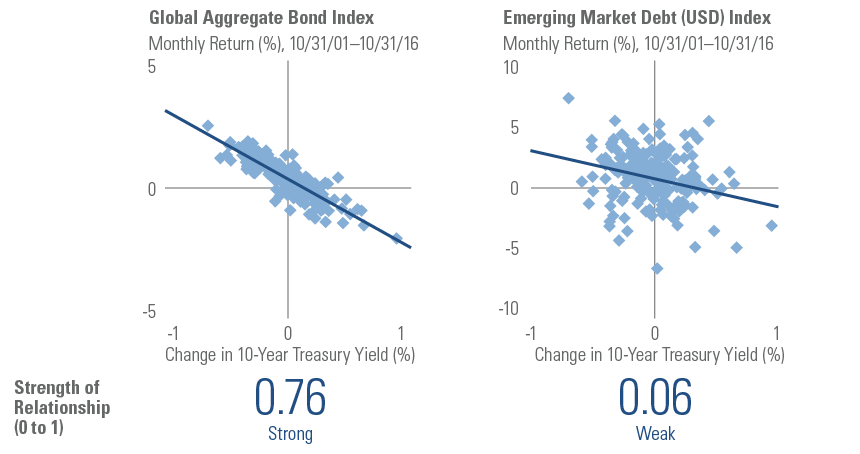

We think the answer is no. While the possibility of nascent protectionism in the US and elsewhere is a risk we are watching closely, we believe fears of emerging market debt (EMD) sensitivity to US rates are overblown. Instead, we think this asset class’ fundamentals are more closely tied to global economic growth and individual country conditions – and that these larger forces may drive both duration moves and EMD performance.

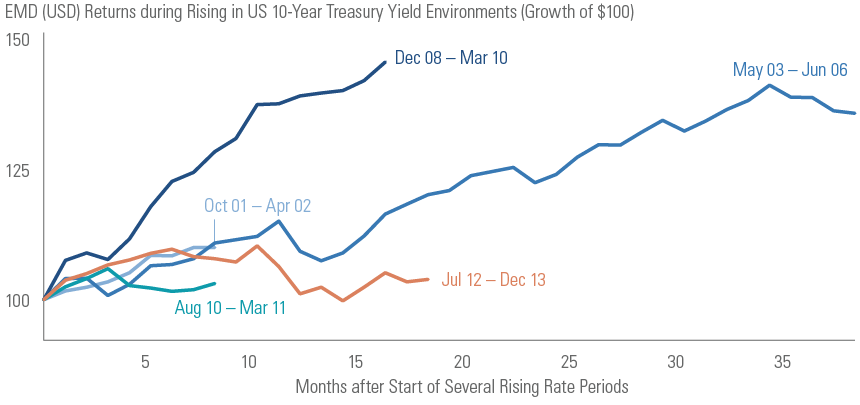

We base that view on the historical performance record, which has not shown much relationship between EMD and rising US interest rates. In fact, as Exhibit 1 shows, the J.P. Morgan EMBI Global Diversified Index, a broad index of US dollar-denominated EMD, has risen in each of 5 rising 10-Year Treasury yield periods since inception.