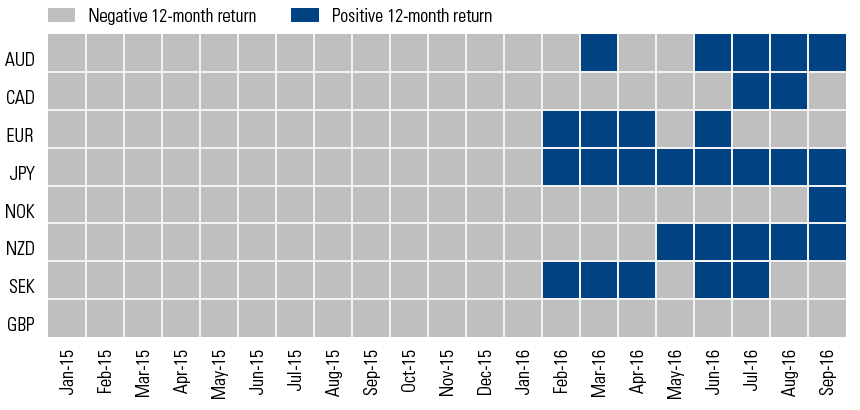

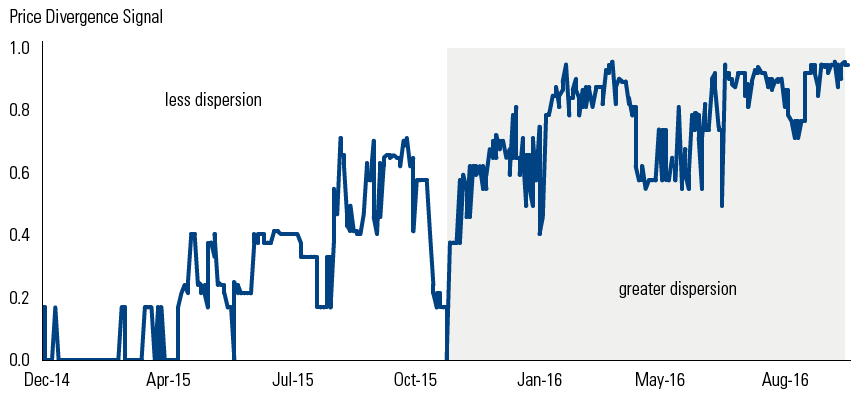

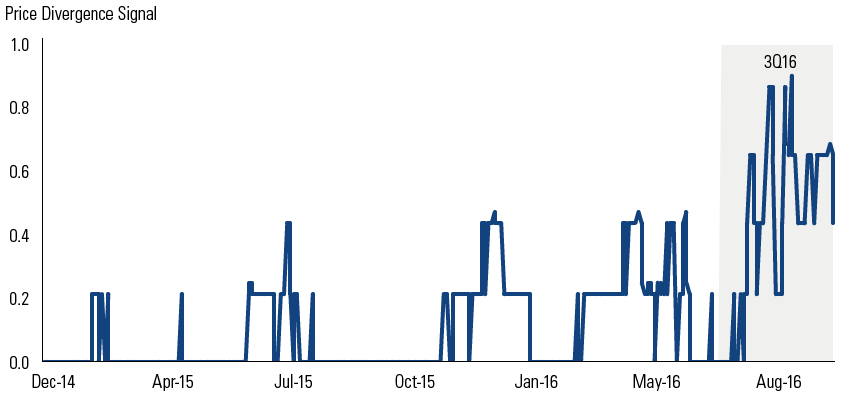

Policy-related market divergence can also be examined by quantitatively analyzing price trends, writes James Park, senior portfolio manager for the Macro Alpha team within GSAM’s Quantitative Investment Strategies platform.

Menu

Our services in the selected country:

- No services available for your region.