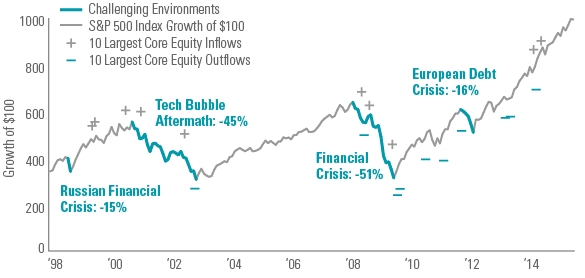

Meanwhile, the months with the largest outflows tell the opposite story. These periods, represented by a “-,“ have often occurred at or near temporary price bottoms, reflecting what we view as periods of unusual pessimism about stocks’ prospects for price appreciation.

The result: Due to decisions made in the heat of market events, many investors have underperformed the very funds they owned.

Specifically, in the decade to Dec. 31, 2014, investors in US equity funds received a pre-tax return that was about 13% lower than the funds in which they invested, according to Morningstar.[1] (The lower “investor return” figure reflects the asset-weighted average 10-year total return, as opposed to the average 10-year total return.)

We believe there is an important lesson in the last 15 years’ history of fund inflows and outflows versus market performance: The value of a long-term mindset. An investor who gained exposure to US equities during each period of a major inflow in the last 15 years would have enjoyed price appreciation had they held on long enough. But both the inflows and outflows suggest that many investors did not heed the old adage about long-term investing.