How can income-oriented investors help their income potential last? We believe a close eye on risk can be crucial. Investors who seek improved portfolio longevity should, in our view, understand the role that lower overall portfolio risk can play in helping portfolios last longer – since lasting longer can mean a greater potential to distribute cash over time. In particular, we would like to highlight the link between lower volatility1 and portfolio longevity.

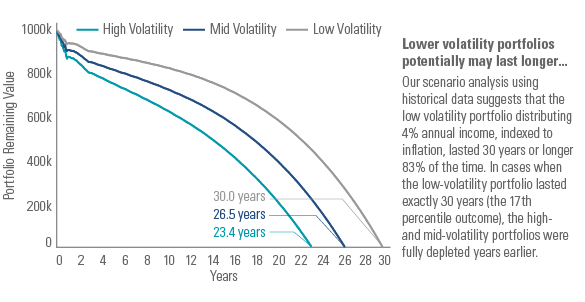

At Goldman Sachs Asset Management, our analysis to illustrate this link (Exhibit One) used historical data to construct millions of potential 30-year investment horizons for portfolios with similar returns, but different levels of risk.

In this analysis, a $1 million “low volatility” portfolio comprised of 55% global equity and 45% global fixed income lasted 30 years or longer distributing 4% annual income more than four out of five times (83% of the time).

In cases when the low-volatility portfolio lasted exactly 30 years (the 17th percentile outcome), we found that higher volatility portfolios were depleted earlier – potentially years earlier – depriving investors of income toward the later years of the portfolio’s lifespan. (The 4% level is used for purposes of illustrating a representative income target level.)

In this analysis, a “mid volatility” portfolio (70% global equities and 30% global fixed income) was, on average, depleted 3.5 years earlier than the low volatility portfolio. And a “high volatility” portfolio (85% global equities, 15% global fixed income) was depleted about six years earlier.

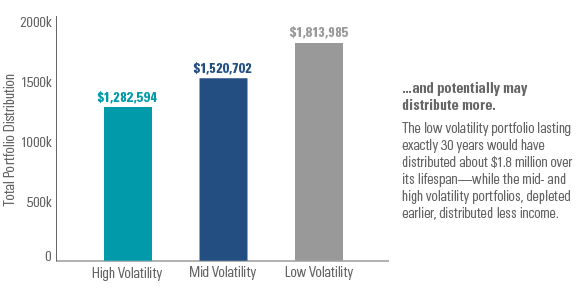

As Exhibit 1 shows, these differing time spans mean that portfolios can deliver markedly different sums of income over their total lives. For instance, the low-volatility portfolio lasting exactly thirty years would have distributed about $1.8 million over the entire time period, while the mid- and high-volatility portfolios, exhausted years earlier, distributed less.

We believe investors should understand the role that risk can play in determining a portfolio’s income potential – especially when it comes to a portfolio’s potential to distribute income over time.