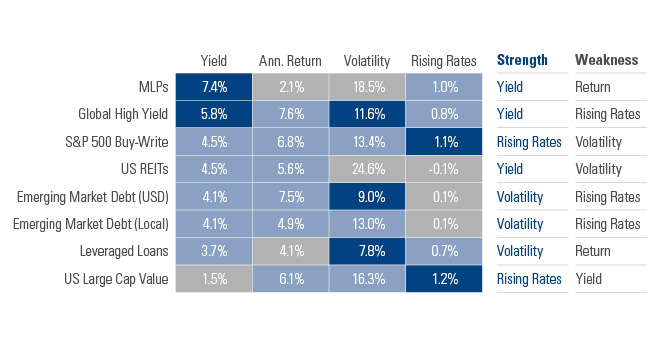

Income-generating asset classes rarely offer the full package of yield, total return, a smooth investment experience, and management of interest rate risks. Instead, as Exhibit 1 illustrates, these asset classes often require tradeoffs between competing goals. The effort to increase yield, for instance, has often come at the expense of higher volatility. Or management of interest rate risk in some cases has required the acceptance of lower yield.

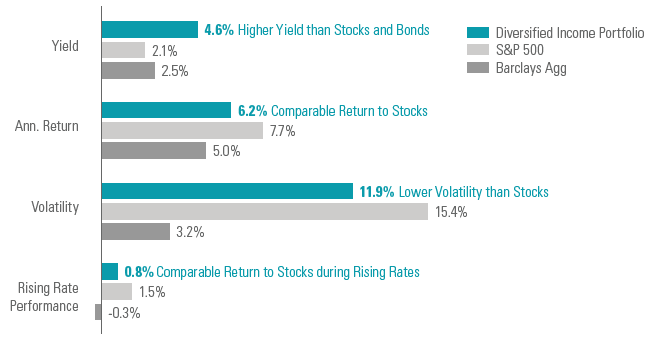

How can investors pursue the income they seek while mitigating these unwanted tradeoffs?