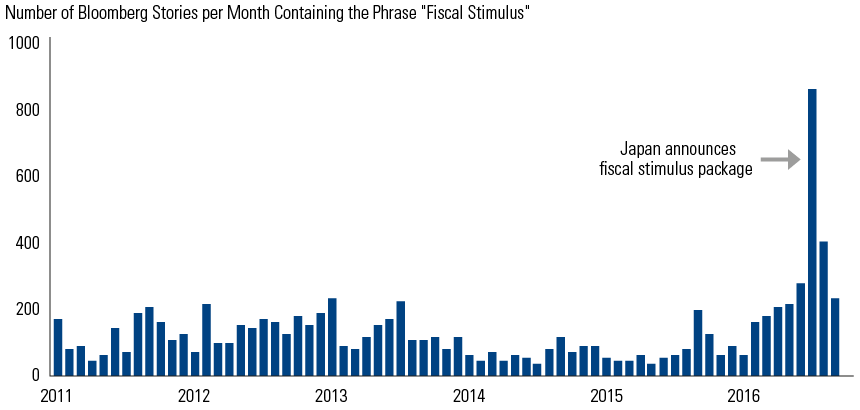

The long recovery from the global financial crisis appears to have reached an important inflection point this year. Monetary policy, the main tool for combatting persistently low growth and inflation, appears close to its limits. As a result, the market’s attention has turned to fiscal policy. In this edition, we attempt to answer some of the questions that arise from this shift.

- What are some of the main challenges facing policymakers? Continued low inflation expectations and growing damage to financial institutions and savers (see Four Charts on Key Policy Challenges).

- What is the outlook? We think monetary policy in Europe and Japan will primarily be about sustaining existing measures, and we see limits to the potential impact of fiscal policy. Our long-term scenarios range from pessimistic (a break-up of the Eurozone) to more optimistic (gradual healing), but we see few near-term catalysts for major market reversals (see Focus).

- Where do markets offer opportunity? We think investors can find selective opportunities in high-yielding stocks, emerging market stocks and fixed income spread sectors (see Focus).

- What are the asset allocation implications? We hold to our view that equities are more attractive than credit and credit is more attractive than interest rates (see Interview).

- What are the implications for divergence? Quantitative trend signals indicate growing divergence in currencies and short-term rates (see Quant Call).